|

|

||||

|

|

||||

|

|

||||

|

|

WHAT'S ON TAP

Container vessel data shows impact of trade war starting to roll in

Is the bear market over?

Auto slowdown weighs on retail sales

Deconstructing the affordable housing value chain

More insider selling from the grocers

Gold ETF sees its 3rd largest daily outflow on record

TRADE WAR MONITOR

It looks like the U.S. isn’t the only one to blink in its dispute with China, with import agencies in Shenzen indicating some of China’s 125% tariffs were quietly rolled back on certain semiconductors and pharmaceuticals.

While we aren’t feeling the impact of the dispute yet, container ship traffic between the two countries has fallen off a cliff, which could create some near-term supply problems if it persists.

HOT OFF THE PRESS

Is the bear market over already?

It’s starting to feel like sentiment is shifting, as markets shrugged off tariff risk last week and focused on the hilariously named Zweig Breadth Thrust (ZWT), a historically bullish signal of broad-based market rallies that flashed last week.

YTD flows into U.S. equity funds have been strong at ~$150B ($250B globally), matching strength seen during the post-pandemic rally.

Retail flows have been strong too, as the segment has been steadily buying weakness for the past 3 months.

As for us, we’re cautiously optimistic. Flows have been strong and broad-based and volatility has subsided, but the macro backdrop is far from perfect and one bad trade headline could put us back where we started.

Auto slowdown weighs on retail sales

Retail sales for February fell by 0.4% M/M (up 4.7% Y/Y), in-line with street expectations and the second straight monthly drop.

Excluding the broad-based softening in auto sales, retail sales would have been up 0.5%, owing to a 2.8% jump in sales at food and beverage retailers.

While preliminary estimates for March are showing a recovery of 0.7%, a long-term recovery will require positive movement on trade.

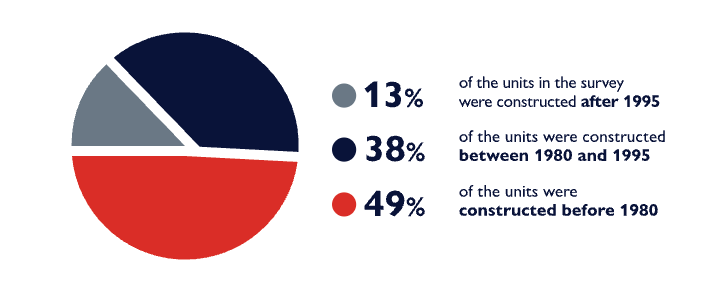

The affordable housing opportunity

We took a pretty thorough look across the affordable housing value chain over the weekend, as we think it will be one of the biggest thematic waves to ride over the next decade - a lot of money could be made here.

We’ve kept it light on words, heavy on visuals, and only available to Morning Meeting readers like you - check it out!

If the above link doesn’t work, try this: https://www.bullpen.finance/content/102

FUNNY BUSINESS

Alright alright, I got the message…

… we’ve taken it a step further and are giving you the option on the website too. Gotta admit, light mode makes it easier to read our long-form work.

If you prefer dark mode, you can use the icon in the top-right to change back. A small upgrade for your reading experience, but we’re pretty excited about some of the bigger things we have coming! Stay tuned.

INSIDER TRANSACTIONS

| Insider | Company | Value |

|---|---|---|

| Daniel McConnell | North West Co. (NWC) | $601K |

| David Chatyrbok | North West Co. (NWC) | $169K |

| Aaron Tonken | Birchcliff (BIR) | $494K |

| Ambrose Bailey | Bausch + Lomb (BLCO) | $136K |

Flagging insider selling at North West Company, as insiders have been selling steadily throughout April.

ON OUR RADAR

GAINERS & LOSERS

|

|

||||

|

|

||||

|

|

TFI International (TFII) reported on the 23rd - the selling is likely more exhaustion from frustrated investors and some institutional re-positioning for this new trade war world.

Hammond Power (HPS-A) is likely just giving some back after a bit of a run - institutional money is quicker to jump out of illiquid stocks in this environment.

EARNINGS

FRIDAY’S EARNINGS

| Company | Actual | Consensus |

|---|---|---|

| 🇺🇸 AbbVie (ABBV) | 2.46 | 2.57 |

| 🇺🇸 HCA (HCA) | 6.45 | 5.80 |

| 🇺🇸 Southern Copper (SCCO) | 1.19 | 1.15 |

| 🇺🇸 Colgate-Palmolive (CL) | 0.85 | 0.91 |

| 🇺🇸 Schlumberger (ABBV) | 0.72 | 0.74 |

TODAY’S EARNINGS

| Company | Time | Consensus |

|---|---|---|

| 🇨🇦 Kraken Robotics (PNG) | AM | 0.01 |

| 🇺🇸 Cadence (CDNS) | PM | 1.58 |

| 🇺🇸 Roper (ROP) | AM | 4.82 |

ECONOMIC DATA

FRIDAY’S ECONOMIC RELEASES

| Release | Actual | Consensus |

|---|---|---|

| 🇨🇦 Retail Sales Ex-Auto | 0.5% | -0.4% |

| 🇨🇦 Retail Sales M/M | -0.4% | -0.4% |

| 🇨🇦 Mftg. Sales M/M | -1.9% | 0.0% |

| 🇺🇸 Consumer Sentiment | 52.2 | 50.8 |

TODAY’S ECONOMIC RELEASES

| Release | Time | Consensus |

|---|---|---|

| 🇨🇦 Wholesale Sales M/M | 7:30AM | - |

| 🇺🇸 Dallas Mftg. Index | 9:30AM | - |

COMMODITIES

|

|

||||

|

|

||||

|

|

||||

|

|

||||

|

|

We’re watching gold closely here, with the GLD ETF seeing its 3rd largest daily outflow on record last week at $1.3B. If the market rebound can hold, appetite for gold may fade as investors rotate back into risk assets.